The January-September 2022 multiple of BFOE crude prices per barrel over CFR Japan naphtha prices per tonne averaged just 7.9. The lowest multiple so far this year was 6.9 in August. The January-September 2022 average was the lowest annual average since our naphtha price assessments began in March 1990.

Asian Chemical Connections

China’s dominance of global polymer demand delivered huge global growth. But what now?

China accounted for 33% of global growth in the seven major synthetic resins between 1990 and 2001. But this jumped to 63% in 2002-2021. In distant second place during both these periods was the Asia and Pacific region at 15% and 17% respectively.

Global PE and PP indexes Week Two: Asian prices recover as Europe declines continue

THESE ARE STILL extraordinary times in global polyolefins markets. Although the great equalisation has begun as pricing in most of the rest of the world falls towards Chinese levels, price premiums over China remain historically very high. There are thus still strong opportunities for exporters to make good netbacks in markets other than China.

European PE and PP producers face re-globalisation risks

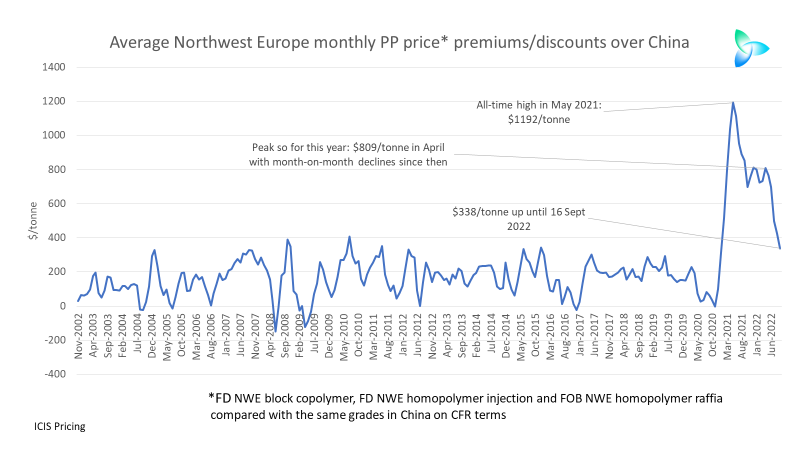

Northwest Europe PP price premiums over China averaged $161/tonne between November 2002 and December 2020. Between January 2021 and 16 September 2022, price premiums averaged $749/tonne. What would be the consequences for European PP pricing and profitability if price premiums returned much closer to their long-term averages?

A perfect global PP storm: China’s collapsing demand and rising capacity

THIS IS A POLYPROYPENE ((PP) world being turned upside down. China has entered a period of lower growth with capacity additions so big that imports are collapsing as China also starts to substantially increase exports.

If you think this is a typical chemicals downcycle, think again

THERE IS A FEELING out there that the chemicals and polymers industry is undergoing a typical downcycle that will last a few years, followed by yet another spectacular fly-up in margins. But I believe a great deal more is happening beyond the usual cycles of over-building followed by under-building.

The rules of the chemicals game are changing as companies pay the penalty for “growth for growth’s sake”

Because companies in all manufacturing and service sectors haven’t been adequately charged for the natural resources they use, and the damage they cause to the environment, we face the risks of catastrophic climate change and more plastic in the oceans than fish.

China PE demand may fall by 5% this year with net imports 3.2m tonnes lower

ANY short-term recovery in China’s PE and PP markets will likely be driven by supply and not demand. Local supply could become tighter on refinery rate cuts. Refineries have reduced production because of weak gasoline and diesel demand.

Global chemicals: What I believe our industry must do in response to a deep and complex crisis

I WORRY that we face a crisis deeper and more complex than any of us have seen before because of the confluence of geopolitics, demographics, the changing nature of the Chinese economy as Common Prosperity reforms accelerate, China’s rising chemicals and polymers self-sufficiency, the high levels of global inflation with all its causes, and, last but certainly not least, climate change.

China goes global in PP perhaps quicker than had been expected, badly disrupting the global industry

CHINA’S polypropylene (PP) industry is in the short- to medium- term is being pushed into going global perhaps quicker than it had intended. This is because of the collapse of local demand and the resulting all-time weak netbacks in China versus most of the other regions.

Jump to page: