Environmental, social and political factors – along with integration into upstream petrochemicals – have held back plant closures. Now, things seems very different.

Asian Chemical Connections

Details of how Saudi Aramco COTC and other advantaged feedstock projects could redraw the petrochemicals map

There is a big new wave of lower-carbon and very advantaged cracker projects on the way, including Saudi Aramco’s crude-oil-to-chemicals investments.

The China and global PP downturns mean CEOs should be asked some tough questions

HOW many PP company CEOs saw this coming, and what their plan now?

Overstocking may have boosted China PE demand as the US continues to win while others lose

THE US gains $296m in China HDPE sales as Asian and Middle East exporters lose $1.4bn.

Winners and losers as demographics, debt, sustainability, geopolitics and crude-to-chemicals rewrite the rules of success

I BELIEVE WE are heading for the biggest period of change in the global petrochemicals industry since the 1990s.

This was when globalisation took off with the formation of the World Trade Organisation (WTO), when China’s economic boom began, when the global population was more youthful and before climate change became a major threat to growth.

China PP demand looks set to grow by just 1% in 2023 as sales losses increase

CHINA’S PP demand could grow by only 1% this year, while major producers saw their January-August 2023 sales in China decline by $796m versus the same months last year.

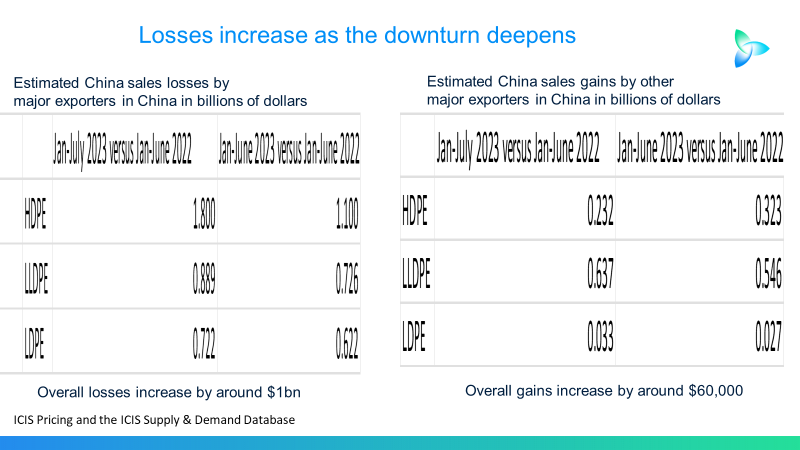

Major PE exporters to China see their sales fall by a further $1 billion

THE BIG PE exporters to China saw their sales to country decline by a further $1bn year-on-year in January-July 2023 versus January-June 2023.

Big HDPE exporters see another $700m of estimated China sales losses in one month

NINE OUT OF CHINA’S top 10 high density polyethylene (HDPE) import partners saw their sales to China fall by an estimated total of $1.8bn in January-July 2023 versus the same period last year. Meanwhile, the remaining member of the top 10, the US, saw its sales increase by $233m.

Global PE capacity may have to be 23m tonnes/year lower in 2023-2030 to end the downturn

GLOBAL PE capacity in 2023-2030 may have to be 23m tonnes/year lower than the ICIS base case to bring markets back into balance

Global HDPE capacity may have to be 13m tonnes/year lower in 2024-2030 to return to healthy operating rates

Global HDPE capacity in 2024-2030 would need to be a total of 13m tonnes/year lower than our base case to return to the 2000-2019 operating rate of 88%.

Jump to page: