In my downside scenario for China’s HDPE demand in 2023-2040 is correct, the country’s total consumption during this period would be 134m tonnes lower than the ICIS Base Case.

Asian Chemical Connections

Why PP producers need to shift from maximising volumes to adding value through sustainability

Why dig more oil and gas out of the ground to make petrochemicals when the carbon cost is potentially ruinous for our climate? This might be a question increasingly asked by legislators, shareholders and the general public – rightly or wrongly.

China HDPE demand set for 3% decline this year with, perhaps, overstocking supporting the other grades

CHINA’S POLYETHYLENE (PE) market has performed in a very mixed fashion so far in 2023, as the above chart tells us.

The annualised January-March 2023 data suggest a 3% fall in high-density PE (HDPE) full-year demand over 2022, a 3% in increase in low-density PE (LDPE) demand and a 4% increase in linear-low density PE (LLDPE) consumption.

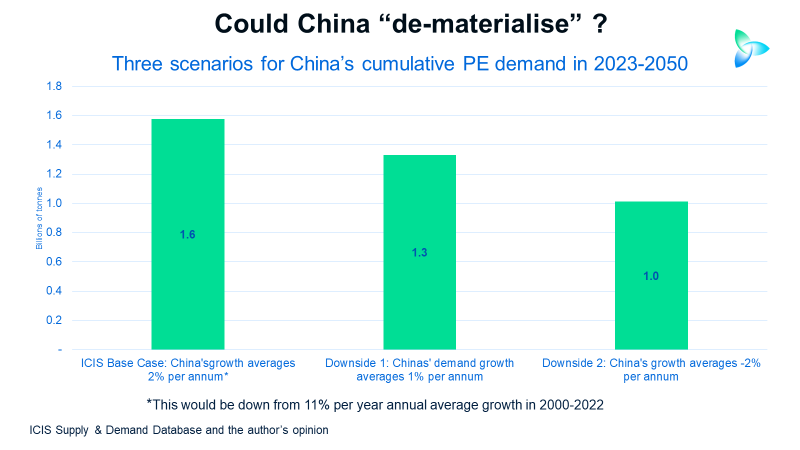

China’s one-off PE demand boom and why consumption could now shrink

The ICIS Base Case is already very conservative, assuming an annual average China PE demsnd growth of just 2% per year between 2023 and 2025 compared with 11% in 2000-2022. But I see average growth of only 1% or even minus 2% as perfectly possible.

Decarbonisation, the timing of the end of this downcycle and building future growth

BECAUSE the old certainties of strong demand growth in China and elsewhere are over, sustainability must be at the core of new petrochemicals growth models.

China PP import and export complexities require much deeper and wider analysis

China’s PP net exports could be more than 2m tonnes in both 2024 and 2025. This would likely make China the fourth biggest exporter in Asia and the Middle East.

China PE and PP downcycle a long, long way from being over

The average China PE spread between 1 January and 17 March this year was just $290, the lowest since our assessments began.

Between 2000 and 2021, before last year’s collapse, the annual spread averaged $532/tonne. This means that until spreads increase by 83% from their current levels, there will have been no recovery..

China’s long-term PP demand growth may turn negative, shifting the focus to value from volumes

STRONG upside PP demand growth scenarios for the rest of the world might still not enough to cancel out negative growth in China

US PE exports in 2023 are not inevitably going to increase

A SCENARIO-BASED approach is essential to understand US PE exports in 2023, based on non-plant economic factors

Why China’s HDPE demand could decline in 2023-2040

China’s cumulative HDPE demand under the downside scenario would be 97m tonnes lower than our base case. in the above chart

Jump to page: